Blade Air Mobility: Business Is Taking Off (NASDAQ:BLDE)

[ad_1]

SerrNovik/iStock by way of Getty Illustrations or photos

Blade Air Mobility (NASDAQ:BLDE) continues to make good progress in the direction of creating a platform for flying taxies. The air mobility platform has viewed business rebound previous pre-Covid ranges, though the inventory has slumped to $5 with the collapse of former SPAC stocks. My financial commitment thesis stays really Bullish on the stock as vacation rebounds to pre-Covid ranges and the market place moves towards eVTOLs that broaden the current market possibility of helicopters.

Asset-Light-weight Small business

In a way, Blade is creating a traveling taxi small business, similar to Uber Tech. (UBER) in the experience-sharing business enterprise. The enterprise is not getting substantial-price plane, loading up the balance sheet with credit card debt, and is just not reliant on any unique eVTOL manufacturer for long term plane. Blade does present the platform to program outings although getting plane time from operators as opposed to Uber employing personal drivers.

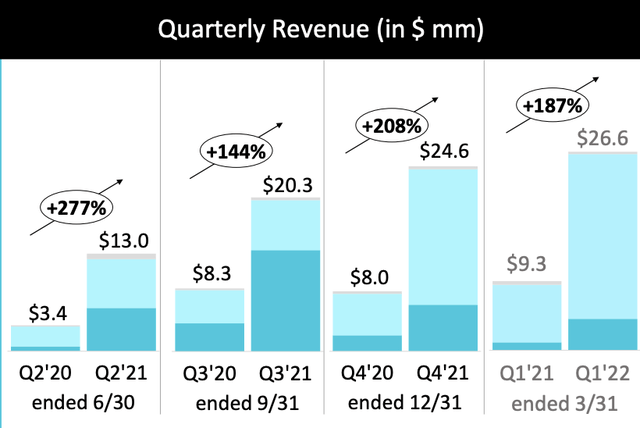

Blade offers the system and the relationship to fliers to make the business operate. For Q1’22, revenues surged 187% to reach $26.6 million. The quantities aren’t as comparable to prior intervals considering Covid absolutely shut down their Blade Airport assistance and the business has created several acquisitions to develop the enterprise.

Source: Blade Q1’22 presentation

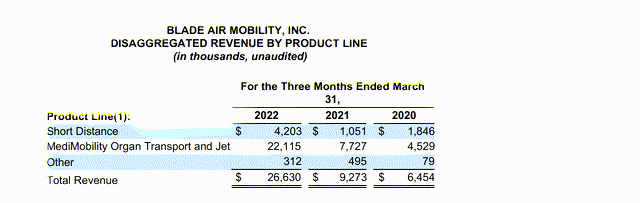

The enterprise has expanded substantially into the professional medical and organ transportation business enterprise with numerous acquisitions. The MediMobility Organ Transport and Jet enterprise jumped to Q1’22 revenues $22.1 million, accounting for over 83% of the small business.

Most traders identify with Blade and the entire city mobility thought primarily based on shuttling fliers about urban facilities or as a assistance for congested airports for lengthy-distance travel. The company has extremely confined existing enterprise from this Short Length category.

The organization finished 2019 with revenues of $5.2 million and described FY19 revenues ending September 30 of $31.2 million. The recent revenue targets have the company reaching the pre-Covid once-a-year concentrations on a quarterly basis due to obtaining the Vancouver procedure and organ transplant business enterprise to build up an expanded air mobility system.

The Blade Airport small business is now achieving new records with an yearly passenger run-amount of 25,000 in the latest weeks. The Small Length small business contains the airport support phase wherever the firm sees a massive opportunity, but the company only generated Q1’22 revenues of $4.2 million.

Source: Blade Q1’22 earnings launch

For Blade to attain the initial projected 2025 revenues of $601 million and 2026 goal of $875 million, the enterprise will have to raise the Shorter Length space by $500+ million. Most of the projected income advancement is not from the MediMobility phase, highlighting how the genuine business enterprise system has not even taken form but. The current addition of 14 more transplant facilities will additional enhance the organ transport section, but the extra business will let the business to reduce flight fees in the quick term.

Path To Earnings

Blade could be out of favor for an prolonged period. The company does not have large margins because of to the asset-mild business design, and the path to gains isn’t shorter.

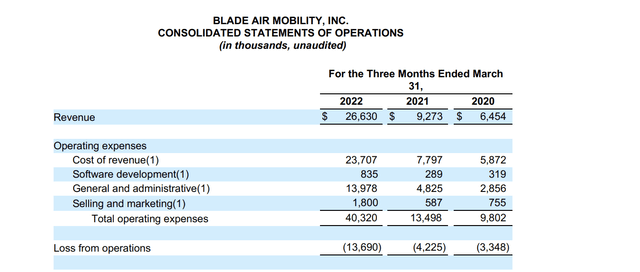

For the quarter, flight margins ended up only 11% thanks partly to the Blade Airport enterprise still in recovery manner. The organization isn’t going to have a significant OpEx foundation, but Blade will will need to drive flight margins up to the specific vary to access the strong EBITDA margins topping 35% in the future.

The OpEx foundation is just in the $16 million range and right after slicing stock-based mostly payment, M&A bills and a single-time lawful costs, the quarterly expense base is substantially nearer to $10 million.

Source: Blade Q1’22 earnings release

The market place cap is down to $473 million (utilizing a thoroughly diluted share rely of 78.8 million centered on 8. million stock selections) after the inventory has been overwhelmed down very similar to other previous SPAC discounts. Blade ended the quarter with the dollars stability at ~$270 million, immediately after burning one more $10 million in income from operations during the March quarter. The stock trades at 3x 2023 income estimates of $160 million, although the EV/S multiple is nearer to 1.5x profits targets. The market definitely hates a “P/S” stock, but these multiples will conclusion up low-priced assuming Blade hits progress targets topping 50% over the subsequent couple a long time.

Naturally, the major threat to the tale is an extended period of time of burning money right before the corporation turns hard cash flow beneficial. Blade is growing in

to Europe, with the opening of Blade Europe in Paris introducing supplemental charges. In addition, important delays in the start of EVAs (electric powered vertical plane) would press out a substantial portion of the industry opportunity exactly where vertical takeoffs from quieter electrical plane are required to unlock additional flights.

Takeaway

The essential investor takeaway is that Blade Air Mobility is establishing a promising air mobility platform, using limited length air transportation to the following degree. The inventory presents an attractive risk/reward situation at the recent selling price, but the upcoming calendar year will be volatile as the organization develops and economic downturn fears loom.

[ad_2]

Source connection