Nation-wide risk of business default worsens as inflation bites: Report

The hazard of default around the following 12 months has amplified in all locations across Australia owing to labour shortages, increasing costs, interest charge hikes, and supply chain troubles.

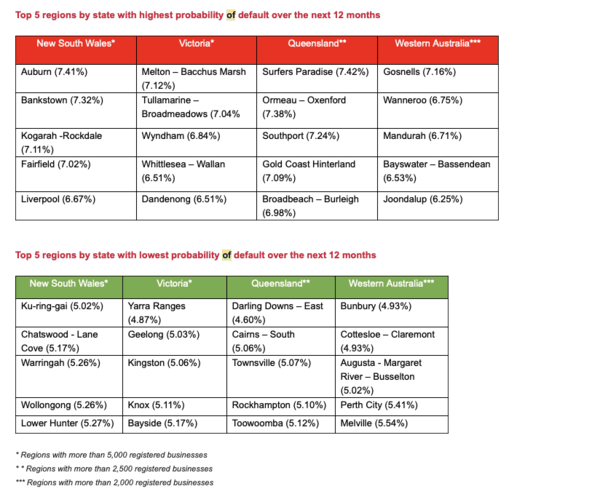

The September 2022 CreditorWatch Organization Hazard Index (BRI) located that the possibility of default more than the next 12 months has developed in all areas across Australia with 5000 or more registered enterprises, apart from New South Wales’ Reduced Hunter and Wyong areas. Organizations are getting a hard time from the east coastline to the west coastline.

Highlights:

- Court steps are up 60 for every cent 12 months-on-12 months.

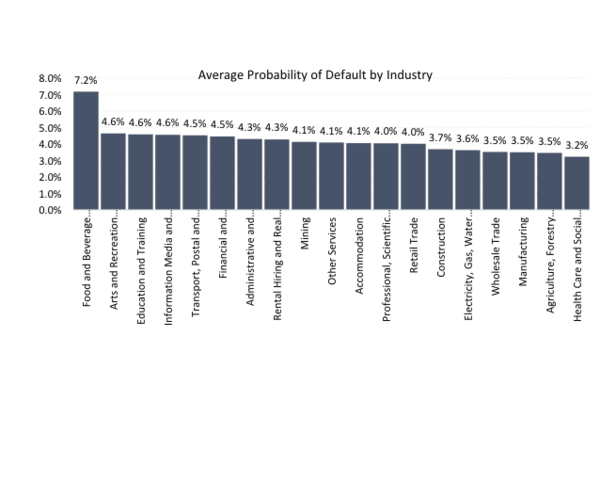

- The industries with the maximum probability of default more than the upcoming 12 months are: Food items and Beverage Expert services (7.20 for every cent) Arts and Recreation Solutions (4.68 for every cent) and Instruction and Schooling: (4.63 for every cent)

Trade activity still down

A more encouraging improvement is that calendar year-more than-yr expansion in B2B trade receivables has continued to rise, which suggests that tiny enterprises’ trade action has ongoing to improve since COVID. Nonetheless, numbers are continue to much underneath pre-covid stages.

Trade exercise has been steadily slipping for some time, but it is now rebounding to more usual stages. The knowledge implies that there are however limitations on how our clientele are impacted by steps that weren’t present right before Covid. These limitations ordinarily come from a absence of products or a protracted hold off in getting them, especially in the building field, as perfectly as labour constraints that prohibit growth or enterprises from performing at entire capability.

Consequently, even even though both countries’ labour force details are however really sparse, the data on open positions indicates that firms’ drive to seek the services of new staff members has lessened. The RBA is obviously staying far more watchful in its method to tightening monetary plan as some indications commence to present that their funds level hikes are starting up to have an influence. It may perhaps take some months prior to this slowdown starts to display up in labour power data.

CreditorWatch CEO Patrick Coghlan stated B2B trade payment defaults confirmed a dip this month however, these stay nicely earlier mentioned amounts seen in September past calendar year throughout Covid and are a guide indicator of upcoming defaults.

“Payment defaults are hugely important and are a important indicator of coming delinquency for the debtor/shopper. Somewhere around 25% of businesses with default conclude up in administration inside 12 months. In addition, it places tension on the provider, who will now have to shoulder that negative financial debt. A company with a trade payment default is seven times the default chance in comparison to a organization with a cleanse payment report.”

The significant photograph

There has been a drop in the benefit of the Australian dollar soon after the central financial institution stunned investors by deciding upon to raise fascination fees by a scaled-down-than-predicted quarter level.

The income charge aim was lifted by 25 foundation points to 2.60 for each cent by the Reserve Bank of Australia. On top of that, it lifted the fascination amount on Exchange Settlement balances by 25 basis factors to 2.50 per cent.

Furthermore, the Abilities Priority List (SPL) uncovered that 286 work opportunities are now in very low offer, up from 153 at the very same time in 2021. Nationally, shortages ranged from apiarists, veterinarians, nurses, and instructors to scaffolders, technicians and trades workers, miners, and landscape gardeners. Resort supervisors, bus motorists, blacksmiths, and magnificence salon administrators are amid the notable new additions to the capabilities shortages.

ALSO Go through: SME sentiment is weakening despite increased profitability. Here’s why

The announcement verifies numerous sector groups’ fears about the long-term skilled workforce scarcity impeding company action across Australia.

Anneke Thompson, Main Economist, CreditorWatch says: “Our Company Risk Index (BRI) information for September 2022 was broadly reliable with data developments we have recorded more than the previous months. Trade Receivables continue to boost yearly, indicating that organizations are however experience fairly self-confident and that provide and labour bottlenecks are little by little clearing up.

“This thirty day period we also observed the Reserve Bank of Australia (RBA) begin to transfer far more cautiously by way of its financial policy tightening cycle, with only a 25 bps maximize in the income charge. Both equally regular monthly Labour Force and quarterly Task Emptiness info that ended up unveiled recently advised that the unemployment rate may have attained its trough.

“The unemployment rate amplified incredibly marginally to 3.5 for each cent, from 3.4 for every cent the thirty day period prior, though the variety of work obtainable decreased by 2 per cent (or 10,000 work opportunities) above the a few months to August. This will be welcome information for company proprietors, most of whom have been struggling to come across employees to satisfy demand. It will also acquire some stress off wage raises. Continue to, work vacancies are at terribly higher stages on prolonged-term actions, and it will take numerous months to normalise.”

As a outcome of mounting gasoline and foodstuff charges, which have achieved a 20-yr large, the Australian economic system is going through issues. This calendar year, the RBA has hiked rates six occasions. Despite the fact that the RBA still left the door open up to much more hikes as it “assesses the prospective customers for inflation and economic growth in Australia.”It claimed that it experienced opted to pause the tempo of tightening because the funds amount had been raised substantially in a short period of time of time.

Way forward

Irrespective of favourable need and trade circumstances for companies at the moment, analysts are nonetheless waiting for customers to really feel the consequences of interest charge improves thoroughly.

There are some early indications that, each domestically and all over the world, company problems have peaked. In accordance to modern Ab muscles Task Vacancy knowledge, there had been fewer jobs obtainable in Australia in August than there were in Could. Related developments may perhaps be noticed in the stats from the US.

So, while labour power knowledge is still really restricted in the two nations, the emptiness information suggests that employment are now beginning to be crammed at a bigger charge, and corporations have slowed their hunger for employees.

It might acquire some months before this slowdown begins to show up in labour power knowledge, but evidently, the RBA is being extra cautious in their strategy to monetary plan tightening as some indicators start off to exhibit that their money price hikes are setting up to just take influence.

Click below for CreditorWatch Business Risk Index report.

Click on here for further insights into the prime and very best performers.

Hold up to date with our tales on LinkedIn, Twitter, Facebook and Instagram.